This article was first published by Colleen Dillenschneider.

Recovery is generally going smoothly for the exhibit-based cultural industry (e.g., museums, zoos, aquariums, gardens, etc.). Though neither exhibit-based nor performance-based institutions are set to completely recover from the effects of the pandemic by the end of 2022 on the whole, intentions to visit are still generally going up and to the right through the end of this year. (Phew!) Thanks to redistribution of demand during the pandemic, things are going particularly well for gardens, zoos, and aquariums as people prefer to spend time outdoors and/or within institutions that allow for greater freedom of movement. These institutions have been realizing comparatively enhanced market potential when compared to the overall exhibit-based organizational average.

But here’s some difficult news: While market potential for the overall industry is still currently estimated to recover to 2019 attendance levels by the end of year 2023, recent findings are challenging this hopeful path.

The research below contemplates 1,981 likely visitors to cultural organizations. The category of “likely visitors” encompasses adults in the US who profile as having any interest at all in taking part in cultural activities and includes both people who already attend (active visitors), as well as those with interest who do not yet participate (inactive visitors). This research aims to understand which activities people intend to do this year (2022) compared to next year (2023).

This research is qualified by intention. We are only asking the question to people who have explicitly told us that they intend to take part in a specific activity that falls within one of these categories. Intention is not the same as interest. Having interest in an activity does not correlate with someone actually doing that activity, although interest is often prerequisite to intention. To have intention to do something means that there is a time-based plan to partake in that activity. For instance, someone may be actively planning their trip to Italy in spring or to visit friends during the summer of 2023.

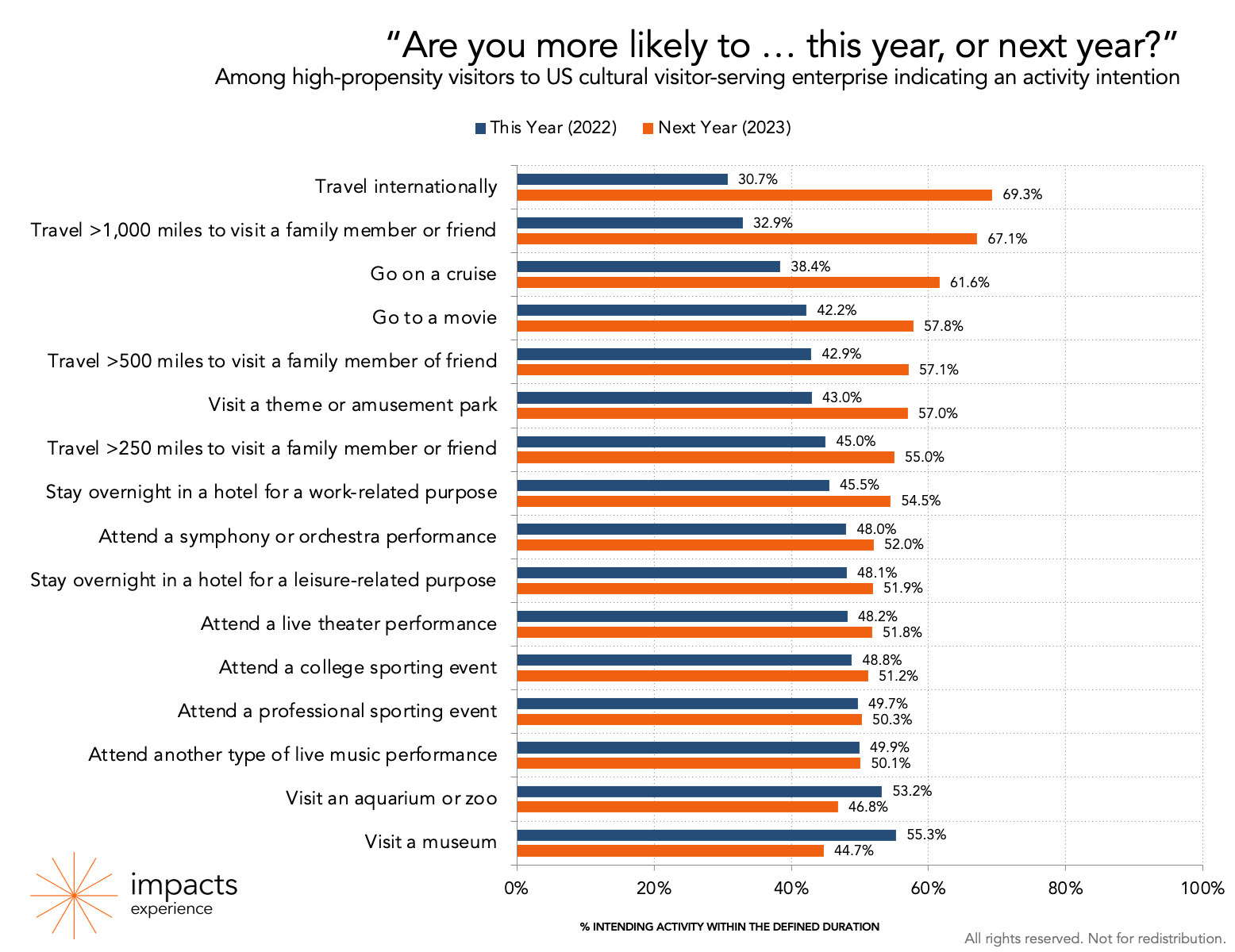

Immediately, you will notice that people currently intend to partake in many of the activities that have experienced a setback during the pandemic in 2023. This includes flying overseas, going on a cruise, attending a theme park – and a whole lot of visiting friends and family!

What does this research mean for cultural entities? Currently, intentions to next attend a live performance remain stable and even increase a bit in 2023, which indicates that this path to recovery may remain steady in terms of competition. This is good news because the last thing performance-based organizations need right now is an added recovery obstacle. However, this is also potentially bad news because the current path to recovery – if it can be realized and negative substitution overcome in the first place – is a slow-burn labor of love for many types of performance-based organizations.

You’ll also notice that likelihood to visit a museum, zoo, or aquarium is lower in 2023 than it is in 2022. If these intentions are realized, this means that market potential may actually be less in 2023 than 2022. Again, these findings haven’t impacted our modeling yet to suggest that this will absolutely be the case, but these are exactly the kinds of inputs with the potential to shake things up.

You can see the goal here: Disrupt the distribution of intentions to partake in various leisure activities – and make it more likely that a museum or cultural organization ends up on the agenda.

Here’s an overview of what’s happening, and what your organization needs to know:

Competition for out-of-home leisure activities is set to increase in 2023

Intentions to visit museums, zoos, and aquariums is predicted to decrease in 2023 while intentions to reengage in vacations and other activities is predicted to increase. This isn’t to say that these institutions haven’t already been aiming to engage audiences mindful of competition, but, instead, that this competition may further grow as people return to the activities that they’ve missed these last few years. This will put an even greater emphasis on the necessity for museums, zoos, and aquariums to highlight their unique differentiators as top-of-mind and desired leisure activities.

Although the chart above shows competition among out-of-home activities, the couch remains a growing competitor. It is a significant one, at that. Needless to say, Americans have gotten used to our sweatpants.

Understanding audiences for successful targeting and re-marketing is critical in 2022

This early finding regarding 2023 puts an emphasis on audience engagement and messaging in 2022. After all, it’s in 2022 that we’re aiming to shake up these intentions and get visiting a museum to be included on the agenda when visiting friends or family.

Despite lower attendance, museums are viewed as more welcoming and attracted more visits from new and emerging audiences during the pandemic because those who live nearby had a reason to visit entities that had otherwise been lower on their to-do list. Now is the time to deliver our A-game in converting those one-time visitors into regular museumgoers. We’ll want to make sure that we are providing our best possible experiences and leveraging positive word of mouth endorsements so that museums remain top of mind throughout the next two years. Providing great messaging and experiences in 2022 can help keep engagement and enthusiasm elevated, and will hopefully shift intentions to visit back toward museums, zoos, and aquariums in 2023.

This includes targeted messaging, strategic programming for new audiences, thoughtful member engagement opportunities, and considering opportunities to become and remain top of mind for local audiences.

Incentivize expired members to re-visit in 2022

Membership renewals are still down for cultural organizations on the whole. Members haven’t let their memberships lapse because they no longer value these institutions, because the cost is too high, or because they don’t appreciate the benefit complement factors such as free admission or supporting an organization’s mission. The primary reason why lapsed members have not renewed is because they intend to do so when they next visit. And they haven’t visited again (yet).

This early findings surrounding visitation intentions suggests that it may be slightly easier to get folks to visit in 2022 than in 2023. If we can entice these lapsed members to return this year, their membership will continue into 2023 and we may then benefit from their presumably positive word of mouth endorsements if/when they visit that same year. If intentions are realized and attendance declines compared when to 2022, it may be especially important to leverage the word-of-mouth endorsement value of our treasured members.

At the risk of teasing readers with data to be published in the coming months, please be thoughtful and cautious when offering discounts on memberships. Promotions are far more successful in cultivating members who are likely to renew than discounts. Discounting memberships can increase member numbers in the short term, sure – but it often comes with deleterious consequences for an organization’s brand, philanthropic efforts, and member numbers in the long term. This is especially the case if an organization discounts its memberships frequently.

Have your admission pricing and business operations in order

Oof. This is a tough lesson from the pandemic, but that doesn’t make it less relevant. If museums are not able to stand up to the competition in 2023, then recovery will take longer, necessitating special consideration to funding and earned revenues over time.

Now is the time to make sure that your institution is charging its data-informed, optimal admission price point. This is a science, not an art. (This is such a fundamental point that it was the topic of my first-ever Fast Facts Video for Cultural Executives!) If revenue is not maximized to keep the lights on, keep people gainfully employed, and if it is not available to reinvest in successful access opportunities, then museums stand to lose their hard-earned ground in expanding audiences.

These are findings to watch. Observing these changes in intentions allows organizations to prepare for possibilities and to work to buck this trend in the immediate near term. It is not the time to despair or accept these intentions as actualized realities yet, but, instead, to work to change them. It’s time to is to hone our game in proving that we are treasured institutions worthy of a visit.

It’s time to outshine the competition – and at least capture a visit when people come to visit friends and family in our respective market areas.

IMPACTS Experience provides data specific to organizations or markets through workshops, keynote presentations, webinars, and data services such as pricing recommendations, market potential analyses, concept testing, and Awareness, Attitude, and Usage studies. Learn more.

We publish new national data and analysis every other Wednesday. Don’t want to miss an update? Subscribe here to get the most recent data and analysis in your inbox.